Structural Steel for Low-Carbon-Emission Lightweight Frames

With global climate change making the conversion of high-emissions extractive processes to circular, sustainable, and resilient processes an increasingly urgent priority, and with professionals, clients, and regulatory bodies all paying serious attention to energy and emissions metrics, improving the performance of this critical industry strikes observers inside and outside the field as a powerful imperative (Muslemani et al.). The relevant metrics include both embodied carbon and operational carbon, though current building codes chiefly address their attention to the latter. These measurements apply to all three scopes of emissions: scope 1 includes greenhouse gas (GHG) emissions from sources that an organization controls directly; scope 2 includes indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling; and scope 3 includes all other indirect GHG emissions resulting from activities in an organization’s value chain (Greenhouse Gas Protocol).

Roughly 42 percent of GHG emissions—an annual total of 36.3 gigatons in direct and indirect energy and process-related CO2 emissions—can be attributed to the built environment, according to architect Edward Mazria’s research and advocacy organization Architecture 2030. Embodied carbon (emissions directly associated with the manufacturing of building materials and building construction) accounts for approximately 11 percent of annual global GHG generation, according to one recent assessment (Carbon Leadership Forum 2020), and for the majority of the carbon emissions associated with global new building and infrastructure between now and 2030 (Architecture 2030). BF/BOF mills can use up to 30 percent recycled scrap in place of extracted iron; with EAFs, the recycled proportion is 100 percent. Steel made in the U.S. currently includes 93 percent recycled content according to the most common estimates, and when used in designs allowing disassembly and separation, it is 100 percent recyclable for future applications.

Replacing BF/BOF methods with EAF worldwide, as North American manufacturers have been doing since the 1980s, is a potent instrument for improving the steel industry’s environmental profile. The global average CO2intensity of BOF production in 2022 was 2.33 tons of CO2 per ton of steel, but only 0.68 tons of CO2 per ton of steel for EAF production (World Steel Association 2023). The industry-wide combined figure, 1.91 tons of CO2per ton of steel, is thus nearly a threefold overestimate of the EAF steel industry’s emission intensity. National steel industries’ environmental profiles vary widely because of rates of EAF adoption, electrical grid conditions, energy sources, the age of facilities, and other factors (Hasanbeigi). Globally, an estimated three-quarters of steel production uses the BF/BOF process, and one-quarter EAF; in the U.S., those figures are essentially reversed.

AISC president Charles J. Carter, SE, PE, PhD, boils the relative footprints down succinctly: “If you buy a ton of steel from China or a ton of steel from the U.S., there’s one-third the carbon in the ton that you’ve bought from the U.S. versus what you get from China. It’s the single thing that a designer could do in the U.S. that would make the biggest impact on sustainability: to require domestic product on a domestic job in the U.S.” Governmental programs supporting domestic green industry such as the Federal Highway Administration’s Buy America program (23 U.S.C 313), the Federal Buy Clean Initiative (part of Pres. Biden’s 2021 Executive Order 14057 on Federal Sustainability), the Buy Clean California Act, and similar initiatives in other states and municipalities thus advance the industry’s emissions-reduction goals. The AISC supports Buy Clean efforts that treat all construction materials equally, offering detailed recommendations for policy makers crafting future Buy Clean regulations (AISC 2022).

“We don't view the steel industry as hard to abate,” says Tim Hill, general manager of sustainability solutions at Nucor, the Charlotte, N.C.-based firm that has become both the largest steel producer and the largest metal recycler in North America. “It’s actually fairly simple. We have the technology; there's one technology right now that can reduce carbon emissions at scale in steel production. It’s just going to be incredibly expensive, because 70 percent of the globe’s steel production relies on a method that is really dirty, and it’s old, and it’s asset-intensive, and a lot of those assets are decades and decades old.”

Because it began operations in the 1960s and embraced EAF technology early on due to its cost-effectiveness, Nucor was able to leapfrog traditional manufacturers’ methods around the time environmental concerns began attaining public prominence. The challenge for other producers and for related professions is to overcome the sunk-costs fallacy that keeps some nations and institutions wedded to BF/BOF, and to transform operations accordingly. Firms including ArcelorMittal, U.S. Steel, Korea’s POSCO and Hyundai, and others, have successfully adopted EAF production along with other clean technologies, regardless of media coverage (e.g., Reed) that overlooks existing green practices, describes steel as a “leading polluter,” and assumes that coke is still universally burned in structural steel production (Swedish firms Svenskt Stål AB [SSAB] and H2 Green Steel have gained publicity as “green steel” makers, joining Indiana-based Steel Dynamics, Boston Metal, Brazil's Gerdau, Nucor, and others in abandoning coke).

The obstacles to that transformation are distinct from questions of differential national development. Not every nation, company, or region can enjoy the leapfrogging timing that benefited Nucor. Although more recently developing economies sometimes outperform older nations or regions in certain sectors (e.g., mobile phones bypassing land-line service in areas where copper-wire infrastructure never appeared, or solar energy bypassing fossil-fuel extraction and dependence), this pattern is less clear in the global steel industry. China, Hill points out, is doubling down on BF/BOF facilities. “As steelmakers across the world are looking for ways to decarbonize their operations, new blast furnace capacity is being added in China, India, and much of Asia. They are not converting current blast furnaces to cleaner EAF technology, but they’re actually building more capacity for old, dirty, inefficient steelmaking.”

Short-term economic decisions that exclude the environmental externalities of emissions and climate disruption make steel appear, from a distant perspective, to be a major part of the problem. Yet in places where EAF production is commonplace, combined with increased adoption of renewable energy sources and design innovations that promote more efficient use of materials, steel is very much part of the solution. Specifying structural steel supplied by an EAF-based source is a choice any environmentally conscientious architect can make in confidence.

GREENING THE ENERGY SOURCES: BEYOND THE BAU-HAUS

Aspects of the domestic steel industry's progress toward sustainability, Bell says, include nationwide use of natural gas rather than coal, increasing shares of renewable energy, and use of direct reduced iron (DRI) along with scrap. Among multiple programs for improving the industry’s carbon footprint, he says, one of the most reliable sources of information is the U.S. Department of Energy's Industrial Decarbonization Roadmap, a comprehensive sector-by-sector analysis of ways for manufacturers to reduce emissions (Department of Energy 2022). Using four scenarios reflecting increasingly aggressive technology and policy improvements—business as usual (BAU), moderate, advanced, and near-zero GHG—the Roadmap identifies increasing the share of EAF steel as the primary way for the nation's steel industry to lower its energy intensity.

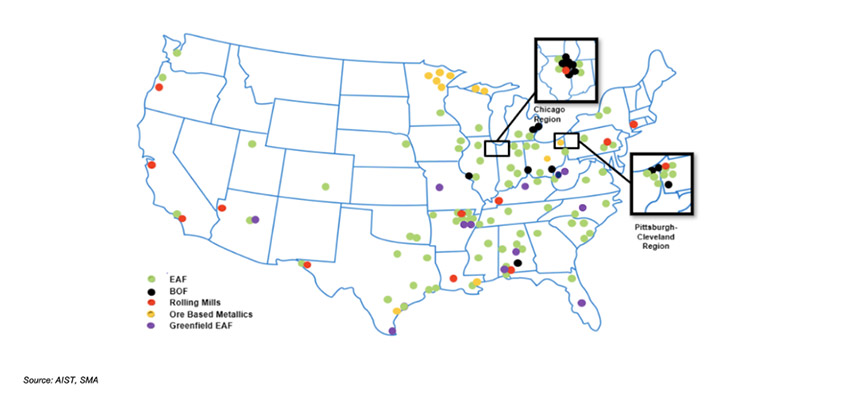

Image courtesy of Steel Manufacturers Association

Figure 3. Geographic footprint of steel facilities in the United States. Source: AIST, SMA

The Roadmap’s prediction that “by 2050, that 90 percent of all steel made in the United States will be made by some other route than integrated steel production or blast furnace steel production,” Bell says, underscores the central role of EAFs in continually upgrading steel’s emissions performance. “If you look at the investments that have taken place between 2021 and are going to go through the year 2025, there’s been over $18 billion in CapEx [capital expenditure] committed or invested in EAF steel production,” he adds, finding concurrence on the importance of EAF steel among “the federal government, the OECD (Organisation for Economic Co-operation and Development), the World Steel Association, and the people with the money.” Most of this investment is by SMA members along with “integrated producers like U.S. Steel, who’s been in the news a lot lately... closing down their blast furnaces and investing in EAF production by acquiring Big River Steel and building a new EAF mill in Arkansas.” (See Figure 3 on the geographic distribution of steel facilities in the U.S.)

U.S. Steel and Nucor are among numerous steelmakers expanding facilities around the nation in response to rising demand and public-sector incentives, along with Steel Dynamics, the currently Russian-owned Evraz (likely to be under new ownership soon, as its part-owner Roman Abramovich is under international sanctions), and Irving, Texas-based Commercial Metals Company (Giusti and Leggate). The recent proposal for Nippon Steel to acquire U.S. Steel may accelerate Nippon Steel’s transition from BF/BOF to EAF facilities; though speculation may be premature because of the contingent status of the sale, Nippon Steel’s position among World Steel’s 2022 Steel Sustainability Champions (World Steel Association 2022) and its declaration of a move toward EAFs and a goal of carbon neutrality by 2050 (Nippon Steel 2023) imply that the firms’ priorities are similarly aligned.

Much of the uncertainty in assessing a product or building’s environmental impact results from scope 3 emissions, which depend on the available power sources, a factor that is only partially under a producer’s control. Houska points out that aluminum plants, which require substantially more energy than steel mills, have often been sited near hydroelectric sources or other sources of cheap local energy. The more alternative energy becomes economically favorable and local electrical systems move from fossil-fuel-based BAU to renewables, the more EAFs will continue to reduce their emissions. More advanced use of alternative energy in European nations, she notes, contributes to low carbon footprints there. In contrast, unreliability of the electrical grid in India, Bell adds, is one of the reasons that nation’s fast-growing steel industry (currently second in the world after China, though not among the top ten a decade ago) has been slow to adopt EAF technology.

In 2018 (the latest date used by the Roadmap for its analyses), natural gas accounted for 37 percent of the U.S. steel industry’s energy use, the highest share among energy types (U.S. Energy Information Administration 2021). Natural gas produces substantially lower emissions per unit of energy than coal and coke, the primary energy sources in China, India, and other BF/BOF-dependent steel producers. Gas is classified as a fossil fuel, carrying risks associated with leaks and drilling, but has a cleaner emissions profile than coal or petroleum. About 117 pounds of CO2 are produced per million British thermal units (MMBtu) equivalent of natural gas, according to the U.S. Energy Information Administration (2022), compared with more than 200 pounds of CO2 per MMBtu of coal and more than 160 pounds per MMBtu of distillate fuel oil. Natural gas is widely (though not universally) defined as a bridge fuel in the national shift toward renewables.

Puchtel summarizes the national energy-source narrative encouragingly: “Over the past 30 years, the U.S. has seen a switch in our power generation, reducing coal-based and increasing natural gas-based. Natural gas, of course, is still a fossil fuel, but it has about half of the carbon footprint that coal-based generation does. So by virtue of the coal numbers and the natural gas numbers flipping over the past 30 years, that's one of the primary reasons why the U.S. electrical grid is relatively much cleaner, both relative to ourselves and compared to the world.”

Hydrogen, Puchtel observes, is increasingly cited as a carbon-free energy source in Europe and the U.S., with some mills outfitted to replace natural gas with hydrogen to fuel reheat furnaces for final shaping and processing of steel. “It seems to be feasible in experiments,” he notes, “but we're still waiting to see it used at scale. The problem with green hydrogen is that once you have it, it’s great, but in order to create it, it takes an enormous amount of energy to do it. And in order for it to be green hydrogen, that enormous amount of energy all needs to be renewable energy.” Hill has observed multiple new technologies using green hydrogen but views them as “in the nascent stage and not economical.... The challenge is, even after you apply the subsidy under IRA (the Inflation Reduction Act), hydrogen is still more expensive than the cost of natural gas.” Bell, likewise, describes hydrogen-based steelmaking methods, reducing iron to DRI for use in the production process, as not yet scalable in the U.S., though European manufacturers aided by government subsidies and investments have made attention-getting headway with it. With Sweden’s Hybrit (Hydrogen Breakthrough Ironmaking Technology), he says, a “fossil-free” DRI steel developed by SSAB, the mining company Luossavaara Kiirunavaara Aktie Bolag, and the energy supplier Vattenfall, “it’s not done on a large scale, and the focus is actually to make flat-rolled steel for the automotive industry, not for the construction sector.”

Notice