This CE Center article is no longer eligible for receiving credits.

Setting Ideal Billing Rates

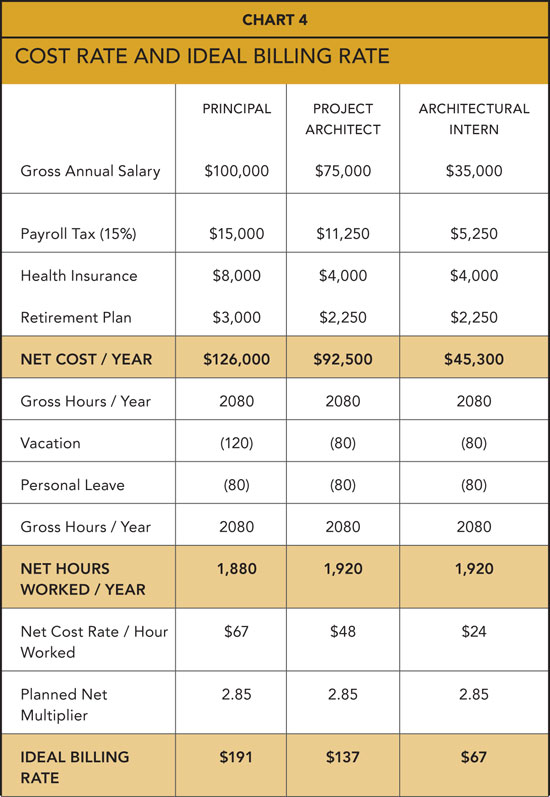

Why is the planned net multiplier so magical? First, it's an incredibly important number to help the firm determine what the minimum hourly billing rates should be for the firm's staff. To show how this works, have a look at each type of staff member in the firm in Chart 4.

So taking into account all the factors for professional salaries and benefits—and how many hours the firm's staff members will work —provides a net cost to the firm for each hour worked. The magical multiplier is then used to get the ideal billing rate. And as long as this architecture office maintains the 65 percent efficiency rate determined earlier, the firm must bill accordingly to get the desired level of profit: the principal at $191/hour, the project architects at $137/hour, and the architectural interns at $67/hour.

Note that in some cases, architecture firms prefer to use an efficiency rate specific to each firm role or job function. So instead of using a “global efficiency rate” for the whole firm, they will evaluate their ideal billing rate for each employee based on their true efficiency levels. (That's a reasonable approach, too, but it's not covered in this learning unit.)

Using these values determined above, the architecture firm can then predict the likely potential value of the employees. This calculation is called the projected realizable income (see Chart 5), and it helps determine a valuable aspect of how the firm must be managed.

The valuable information is also good news: It shows that at the firm's planned billing rates, the potential income is greater than planned. Specifically, the total realizable income of $627,200 exceeds the $500,000 projected in the firm's profit plan. So the firm could invoice 80 percent of its potential and still hit the goals set forth in the profit plan.

It sounds like good news, and actually it's typical, according to experts in architecture firm management. This is a very common position for most firms, and they obviously would like to bill the full potential of the staffing and predicted efficiencies. Considering that the principal will be spending half of his or her time working on non-billable things, we would hope that these efforts are what will continue to bring new work into the firm.

Summarizing the key data required to run a financially successful firm, the Houston-based management consultant Steve L. Wintner, AIA, listed 10 key indicators in his AIA best-practices article, “Financial Management: 10 Key Performance Indicators”:

▶ 1. Utilization rate. As reviewed above, the utilization rate is not a measure of efficiency, but rather the percentage of hours spent on billable projects out of total available working hours. It is not a measure of productivity. “A reasonable goal for the entire staff would be a utilization rate of 60 percent to 65 percent,” wrote Wintner, the founder and principal of Management Consulting Services, Houston, “and for professional and technical staff—including principals—a reasonable goal would be 75 percent to 85 percent.”

▶ 2. Overhead rate. Comparing the cost of expenses not related to projects as a portion of total direct labor gives a percentage, which is the overhead rate. This rate must be known in order to determine an architecture firm's profit. Low is best for this rate. Wintner cautions that if the overhead rate is greater than 1.75 times total direct labor, the firm should immediately consider corrective actions.

▶ 3. Break-even rate. Just add 1.0 to the overhead rate and that's the firm's break-even rate. For example, if the overhead rate is in the danger zone of 1.75, the firm must earn $2.75 for every $1.00 it spends simply to break even. Wintner observes that each firm employee has a break-even cost: “the overhead rate plus each person's hourly salary.” So the break-even rate for the example above is 2.75 times the hourly salary, which for the $24.00 per hour intern in the example on the previous page, would be $66.00 per hour—just to break even on the intern's work.

▶ 4. Net multiplier. This compares firm revenues as a portion of total direct labor. It should be greater than the break-even rate—because that means the firm is profitable!

▶ 5. Profit-to-earnings ratio. If an architecture firm is effective at completing building projects profitably, they should have a higher profit-to-earnings ratio. To calculate the firm's profit-to-earnings ratio, just divide the pretax profit by net operating revenue.

▶ 6. Aged accounts receivable. Invoices should be paid as fast as possible. Within 60 days is typical, and anything beyond that should be addressed immediately. The measure aged accounts receivable helps identify the average age or length of time accounts receivable are outstanding. To calculate it, first divide the firm's net operating revenue by 365 days. Then take the last 12 months of accounts receivable to get the average annual figure, and divide this by the daily net operating revenue figure just calculated previously. In other words:

Average annual unpaid fees ÷ (net operating revenue ÷ 365)

Image courtesy of BQE Software

For a work in progress, the measure of aged accounts receivable helps identify the length of time invoices remain unpaid.

▶ 7. Proposals pending. On the other hand, a firm can review its strengths and weaknesses at creating winning proposals—and more importantly, generating enough proposals to earn enough future revenues. This calculation includes prospects, says Wintner, which are “proposals that the firm has a 50 percent or better chance of winning,” as well as suspects, where the proposals are estimated “to have a chance of winning of less than 50 percent.” Add up the total dollar amount of prospects and suspects and compare the total to annual net operating revenue: Proposals pending should be about 2.5 or three times net operating revenue—with the caveat that prospects run at least equal to net operating revenue and suspects at about 1.5 to two times net operating revenue.

▶ 8. Backlog volume. Another good measure of a firm's short-term business robustness is backlog volume, the unbilled portion of current contracts. Monthly invoices are a good thing, of course, but they also erode backlog volume. To stay healthy, a firm wants to replace any fees invoiced with newly contracted fees. Wintner and other experts advise that savvy firms push hard to keep their backlog volumes at least equal to annual net operating revenue, if not much greater.

▶ 9. Net revenue per employee. Easy and revealing, too: Just divide annual net operating revenue by the number of employees. This measure helps to predict future yearly net operating revenue, says Wintner, who has been a licensed architect since 1968 and also past chair of the AIA Practice Management Committee.

▶ 10. Cash flow. For architecture firms, cash flow is what separates the great-struggling firms from the great-successful firms. It's worth a detailed discussion.

Managing a successful architectural practice relies on a number of immutable, longstanding truths. Yet there's an equal influence of new trends, techniques, and tools that separate the reasonably well-run firms from those that excel. In part, the more recent advances in firm financial management relate to macro trends in the field, according to the American Institute of Architects' (AIA) recent Firm Survey Report. For example, while about half of all U.S. firms were registered as sole proprietorships just 15 years ago, today that share is only about 20 percent.

Yet even the smallest firms—those with fewer than 10 employees—earn a large share of the national total of architectural billings, at about 20 percent of the total according to the AIA survey. Expand the sample to firms with up to 20 employees, and you have the lion's share of billings. That's millions and millions in revenue for these firms, and a key reason to keep careful tabs on firm financial operations.

“Providing great architectural services and running a financially successful firm are not mutually exclusive,” says Steven Burns, FAIA, former principal of Burns + Beyerl Architects and now chief creative officer at BQE Software Inc. “It's quite the contrary. What separates the great-struggling designers from the great-successful designers isn't luck. The latter practitioners understand the rules of the game and wield them to the benefit of their firms, their projects, and their clients. And clients are attracted to winners, too.”

Part of what makes great and successful design firms is purely organizational. These firms are able to quickly and efficiently provide principals, project managers, and entire staff essential information they need. They've reduced the amount of time needed to manage project tasks, billings, and documentation so that they have more energy and creativity for the core activity: design workflow.

Their invoicing is clear and meets client expectations. They're using the leading edge of technology to automate processes, manage tasks and phases, eliminate misfiled documents, and run reports easily and quickly.

Photo courtesy of Looney Ricks Kiss

For smaller firms as well as for larger firms, such as Looney Ricks Kiss, based in Memphis, best practices in firm financial management are essential to long-term success.

“We are a small firm of seven that was using separate software programs for billing, time tracking, contact management, and calendaring,” says Donald Powers, AIA, principal of Union Studio in Providence, Rhode Island. The approach was inefficient and time-consuming, he adds. By focusing on project flow and formalizing firm management practices with a new financial software platform, Powers has since implemented comprehensive templates for correspondence and project administration as well as automated billing summaries. In addition, all the firm's designers enter their own time into a central database to simplify invoicing.

Image courtesy of BQE Software

There is complexity in managing any A/E company’s finances, so many firms use automated systems and software that can churn out answers immediately.

A similar turnaround helped the San Francisco firm BRU Architects reduce their invoicing turnaround and automate staff payroll and vacation tracking. “It used to take us months to get invoices out,” says Rebecca Firestone, the firm’s former manager of business operations. After adopting the new practices and systems, “invoices would usually go out within five days of the last month’s cutoff, and the amounts were definite and easily auditable.”

Every firm wants to share a story like this. So where should they start?

Choosing to Make Money

It's not an architect's fault that after all the years of education and training one must endure to become an architect that the resulting firm leader doesn't know the first thing about how to run a business. But in addition to designing and detailing structures, the architect who is a firm leader must also truly understand the difference between income and revenue, and between a credit and debit, just to name two key pairs of accounting terms. The firm leader has to know what a minimum billing rate and an overhead factor are, and why these two measures are so critical to successful practice management.

“In the end, understanding financial management is like understanding building codes or doing a zoning and code analysis,” says BQE's Burns. “Even though you think you understand everything—for example, because you did a similar project before—it's essential that you stop and go through the entire process.”

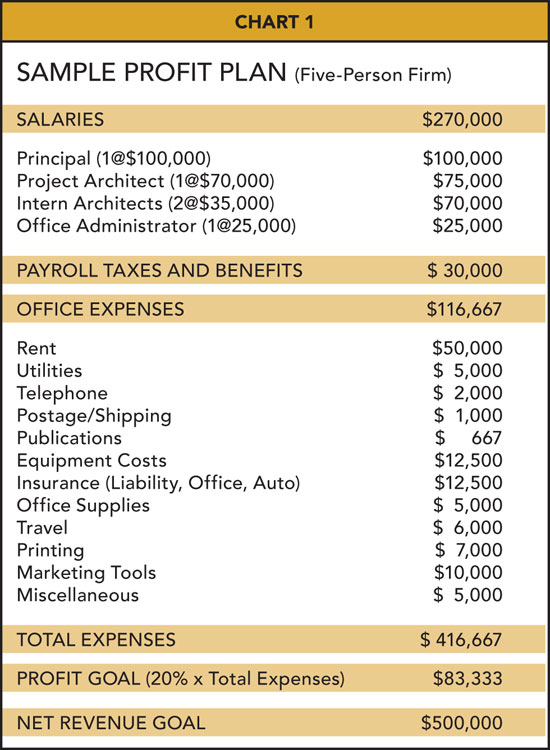

According to the AIA publication The Architecture Student's Handbook of Professional Practice, firm financial planning can be described as a six-step process. Starting out the full analysis, an architecture firm's financial health is best considered by looking at the firm's estimated operating budget—also known as a profit plan. “Financial guideposts come from a profit plan,” according to the AIA textbook. A simple, essentials-only version of a profit plan follows, which is helpful to any small or emerging firm. The plan is based on three steps:

▶ 1. Estimating expenses. This includes the firm's salaries and benefits as well as payroll taxes. It also includes approximate office expenses but not client reimbursable expenses or consultant project fees that are passed through to the client.

▶ 2. Establishing a profit goal. This may also be described as the firm's return on investment (ROI), and is usually stated as percentage of net revenues, after expenses and before taxes. All the effort and money the firm puts into its business should return a profit. This is what one would expect if money were invested in something else, such as stocks, bonds, or real estate.

What's the return a small or emerging firm should expect? Burns recommends 20 percent, while some management consultants offer targets in the range of 15 percent to 25 percent. “Architects pour their life into these building projects, so the return should be commensurate with the effort,” says Burns. “Otherwise, they might as well take the money and invest it in the stock market.”

▶ 3. Determining the net revenue goal. The estimated expenses are added to the profit goal, which is given as a dollar figure based on projected or desired gross revenues. This totals up as the net revenue goal. It's a net figure because it omits all reimbursable expenses listed earlier. The net revenue goal has another important function in the life of an architecture firm: It represents what the firm plans to invoice clients for their architectural services rendered. In the sample profit plan shown below, the net revenue goal is $500,000.

So the net revenue goal is known: a cool half-million. Now that the firm has established its targeted net revenue at $500,000, the firm leadership needs to understand from where this revenue is derived.

Reaching the Firm’s Profit Goals

Architects earn their revenue (and profit) by working on building projects. So it should come as no surprise that the most common denominator for planning and measuring financial performance is the direct salary expense (DSE). This is the salary cost of the hours charged to projects—in other words, the firm's billable time. Knowing the staffing level and overhead, a firm's profit goal can be used to determine how much direct salary must be charged in order to hit that profit target at the end of the year, according to the AIA publication, The Architect's Handbook of Professional Practice.

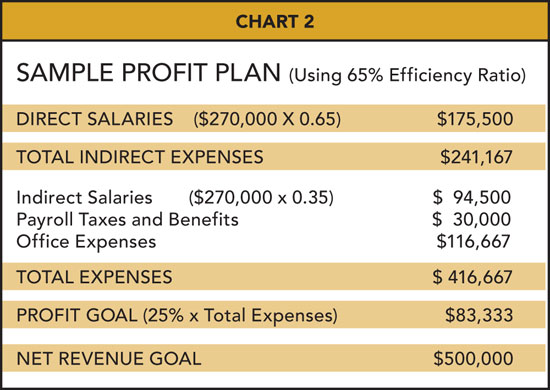

To illustrate, the firm can apply the sample profit plan developed above to calculate the DSE multipliers, which are numbers that can be used to determine the values such as the target break-even, profit, and revenue amounts. But in order to do this, the firm must first determine its Efficiency Ratio. The efficiency ratio is calculated by dividing direct salary expense by total salary expense. This also means that:

Direct Salary Expense = Total Salary Expense x Efficiency Ratio

So how does an architecture firm determine its efficiency ratio? They can do the math above, or they can assume a profession-wide benchmark. For example, there are statistical surveys showing that, on average, architectural firms achieve about 65 percent efficiency ratios. This averages all employees—not only principals but also all staff members—even though efficiency ratios may be different for principals than they are for interns or others. For example, national benchmarks show that principals may be only about 50 percent efficient, for example spending 20 of their 40 hours/week on work billable to projects, while architectural interns may be 95 percent efficient.

Armed with this information and the resulting ratios, the firm can modify the sample profit plan above by making adjustments to acknowledge the estimated efficiency ratio:

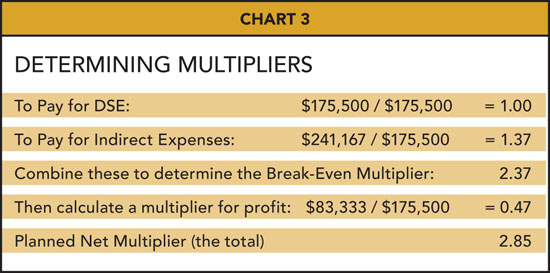

Using the results from Chart 2, the firm knows that its total salary is $270,000. But since it operates only with a 65 percent efficiency ratio, the firm's DSE or direct salary expense is $270,000 x 0.65, or $175,500. Next, the firm must determine its break-even multiplier (determined by dividing direct labor plus overhead by direct labor) and its planned net multiplier, a measure of the revenue required for each dollar of direct labor spent on projects.

Adding together the multipliers for the firm yields the planned net multiplier—in this case, of 2.85. Like a utilization rate, this is a measure of the firm's efficiency at producing work and yielding a profit. And this is a magic number, specific to the firm. Once the firm knows it, they can make a number of financial planning decisions.

Setting Ideal Billing Rates

Why is the planned net multiplier so magical? First, it's an incredibly important number to help the firm determine what the minimum hourly billing rates should be for the firm's staff. To show how this works, have a look at each type of staff member in the firm in Chart 4.

So taking into account all the factors for professional salaries and benefits—and how many hours the firm's staff members will work —provides a net cost to the firm for each hour worked. The magical multiplier is then used to get the ideal billing rate. And as long as this architecture office maintains the 65 percent efficiency rate determined earlier, the firm must bill accordingly to get the desired level of profit: the principal at $191/hour, the project architects at $137/hour, and the architectural interns at $67/hour.

Note that in some cases, architecture firms prefer to use an efficiency rate specific to each firm role or job function. So instead of using a “global efficiency rate” for the whole firm, they will evaluate their ideal billing rate for each employee based on their true efficiency levels. (That's a reasonable approach, too, but it's not covered in this learning unit.)

Using these values determined above, the architecture firm can then predict the likely potential value of the employees. This calculation is called the projected realizable income (see Chart 5), and it helps determine a valuable aspect of how the firm must be managed.

The valuable information is also good news: It shows that at the firm's planned billing rates, the potential income is greater than planned. Specifically, the total realizable income of $627,200 exceeds the $500,000 projected in the firm's profit plan. So the firm could invoice 80 percent of its potential and still hit the goals set forth in the profit plan.

It sounds like good news, and actually it's typical, according to experts in architecture firm management. This is a very common position for most firms, and they obviously would like to bill the full potential of the staffing and predicted efficiencies. Considering that the principal will be spending half of his or her time working on non-billable things, we would hope that these efforts are what will continue to bring new work into the firm.

Summarizing the key data required to run a financially successful firm, the Houston-based management consultant Steve L. Wintner, AIA, listed 10 key indicators in his AIA best-practices article, “Financial Management: 10 Key Performance Indicators”:

▶ 1. Utilization rate. As reviewed above, the utilization rate is not a measure of efficiency, but rather the percentage of hours spent on billable projects out of total available working hours. It is not a measure of productivity. “A reasonable goal for the entire staff would be a utilization rate of 60 percent to 65 percent,” wrote Wintner, the founder and principal of Management Consulting Services, Houston, “and for professional and technical staff—including principals—a reasonable goal would be 75 percent to 85 percent.”

▶ 2. Overhead rate. Comparing the cost of expenses not related to projects as a portion of total direct labor gives a percentage, which is the overhead rate. This rate must be known in order to determine an architecture firm's profit. Low is best for this rate. Wintner cautions that if the overhead rate is greater than 1.75 times total direct labor, the firm should immediately consider corrective actions.

▶ 3. Break-even rate. Just add 1.0 to the overhead rate and that's the firm's break-even rate. For example, if the overhead rate is in the danger zone of 1.75, the firm must earn $2.75 for every $1.00 it spends simply to break even. Wintner observes that each firm employee has a break-even cost: “the overhead rate plus each person's hourly salary.” So the break-even rate for the example above is 2.75 times the hourly salary, which for the $24.00 per hour intern in the example on the previous page, would be $66.00 per hour—just to break even on the intern's work.

▶ 4. Net multiplier. This compares firm revenues as a portion of total direct labor. It should be greater than the break-even rate—because that means the firm is profitable!

▶ 5. Profit-to-earnings ratio. If an architecture firm is effective at completing building projects profitably, they should have a higher profit-to-earnings ratio. To calculate the firm's profit-to-earnings ratio, just divide the pretax profit by net operating revenue.

▶ 6. Aged accounts receivable. Invoices should be paid as fast as possible. Within 60 days is typical, and anything beyond that should be addressed immediately. The measure aged accounts receivable helps identify the average age or length of time accounts receivable are outstanding. To calculate it, first divide the firm's net operating revenue by 365 days. Then take the last 12 months of accounts receivable to get the average annual figure, and divide this by the daily net operating revenue figure just calculated previously. In other words:

Average annual unpaid fees ÷ (net operating revenue ÷ 365)

Image courtesy of BQE Software

For a work in progress, the measure of aged accounts receivable helps identify the length of time invoices remain unpaid.

▶ 7. Proposals pending. On the other hand, a firm can review its strengths and weaknesses at creating winning proposals—and more importantly, generating enough proposals to earn enough future revenues. This calculation includes prospects, says Wintner, which are “proposals that the firm has a 50 percent or better chance of winning,” as well as suspects, where the proposals are estimated “to have a chance of winning of less than 50 percent.” Add up the total dollar amount of prospects and suspects and compare the total to annual net operating revenue: Proposals pending should be about 2.5 or three times net operating revenue—with the caveat that prospects run at least equal to net operating revenue and suspects at about 1.5 to two times net operating revenue.

▶ 8. Backlog volume. Another good measure of a firm's short-term business robustness is backlog volume, the unbilled portion of current contracts. Monthly invoices are a good thing, of course, but they also erode backlog volume. To stay healthy, a firm wants to replace any fees invoiced with newly contracted fees. Wintner and other experts advise that savvy firms push hard to keep their backlog volumes at least equal to annual net operating revenue, if not much greater.

▶ 9. Net revenue per employee. Easy and revealing, too: Just divide annual net operating revenue by the number of employees. This measure helps to predict future yearly net operating revenue, says Wintner, who has been a licensed architect since 1968 and also past chair of the AIA Practice Management Committee.

▶ 10. Cash flow. For architecture firms, cash flow is what separates the great-struggling firms from the great-successful firms. It's worth a detailed discussion.

Architecture Firm Cash Flow

Some firms look profitable and successful—and their principals like that feeling. Yet they may still have cash-flow issues from time to time, when bills are running high for its pass-through reimbursables and other expenses while a few clients may be taking longer than expected to settle their invoices.

Cash management, or cash-flow management, is a valuable competency for any professional services firm—architects included. According to Peter Piven, FAIA, the Philadelphia-based principal consultant of the Coxe Group, Inc., a marketing and management consulting firm for design professionals, “The best tool for addressing these questions and evaluating firm solvency is cash budgeting,” a targeted technique to forecast projected cash flows moving into a firm—and out of the firm—over a period of time.

Photos courtesy of BQE Software

Regardless of firm size or project scope, cash-flow management is indispensable for evaluating the firm’s solvency.

To take advantage of cash budgeting, the firm needs to draw together a variety of reports and data on forthcoming cash receipts and expected payments. The results will help show expected surpluses and shortfalls of funds, Piven writes in his recent essay, Maintaining Financial Health. Done properly, it will also indicate needs for short-term borrowing and, in some cases, the capacity to invest excess cash. According to Piven, there are basically five or six essential steps required for the cash budgeting process:

▶ 1. Forecast billings. This requires a look forward at the firm's projects and prospects, and making an accurate and conservative assessment of what the firm can bill.

▶ 2. Forecast cash receipts from billings. This should include the amounts and timing of collections from the billings anticipated above.

▶ 3. Forecast cash receipts from other sources. Some design firms earn royalties on their furniture designs, for example, and their timing may be less predictable. Other cash revenue sources may include sales of assets such as a printer or property, or income from firm investments.

▶ 4. Forecast cash disbursements, as Piven explains, that must consider “payroll, consultants, other direct (project) expenses, indirect (overhead) expenses, reimbursable expenses, and capital expenditures.”

▶ 5. Combine the schedules for cash receipts and cash outlays. This provides a matrix of forecasted figures.

▶ 6. Calculate the results. With the combined data, a net figure indicating a cash increase or decrease can be determined for each month up to the forecast horizon. The beginning cash balance provides a baseline for determining the firm's cash position for each of the forecast months.

Piven also outlines best practices in cash flow controls, which correlate with many of Wintner's assertions on what any architect should know to run a financially successful firm. “Controlling cash flow requires measuring actual performance against the budget and taking corrective action as needed,” according to Piven. With this in mind, the managing partners should focus on keeping backlog numbers healthy—by getting more projects and keeping existing projects on track—and by sending clients accurate, auditable bills that they expect and understand. Other key steps include watching cash receipts and using collections methods as needed, and working on ways to control commitments and outlays of cash. Most important, perhaps: Piven says firms should calculate their cash budgets often and actively use them for their purpose—as a way to keep an eye on cash flow.

Using Financial Systems to Keep Firms Profitable

Once you have trustworthy cash projections, the firm can be more nimble and adaptable to changing financial and economic conditions, Wintner writes, because cash-flow tools “can help a firm plan ahead to smooth out the swings in cash flow by accelerating collections, requesting an initial payment prior to starting a project, and carefully planning purchases of equipment and supplies.” Wintner also cautions that some firms may see a “habitual dependence on a line of credit,” which usually indicates structural problems with the firm's financial situation.

As the cash flow budgeting process shows, there is a certain minimum level of complexity to managing any professional service firm's finances, even if it's a three-person architecture-and-interiors practice. Drawing up a monthly cash-flow report takes time and access to all the required data. A 12-month projection takes a bit of math, but many firms use automated systems and software that can churn out the answers immediately—if the data entered is reliable.

“The cash-flow example opens the door to a discussion of the practical aspects of financial management,” says BQE Software's Burns. “These are the day-to-day things that really need to happen in any architectural firm, no matter how small.” Key management competencies required for all firms—and the associated software and hardware for automating these efforts—include:

▶ Accounting. “This may be obvious, but all firms need some form of accounting software,” says Burns, noting that a number of effective and inexpensive accounting products are on the market. “Choose an accounting software that is both highly affordable and scalable.” If possible, the base financial accounting software should be backwards-compatible with any other accounting systems that have been used in the firm.

When used properly, the accounting products serve as an effective tool to help principals understand their own businesses. It also provides a single platform for managing the company's basic accounting needs, such as taking care of the bills owed (accounts payable), and to efficiently run common financial reports, such as the balance sheet and income statement.

▶ Payroll. The accounting software product is also used to handle payroll. However, once the architecture firm reaches a certain size—typically 4-5 people employed, or more—many firms choose to migrate to an outside payroll system vendor. There are many of these companies on the market, and even the largest international vendors work with very small businesses.

The fees charged by payroll service providers vary, so the firm should do some initial research before selecting the best payroll company for the firm. Note that they can do a lot more for the firm than just payroll, such as preparing reports. They are also responsible for making sure payroll taxes and benefit contributions are paid on time, so the firm is never penalized for late payments. “It takes the burden away from you, the firm owner, so you can focus on what you do best,” says Burns.

▶ Project management. One of the reasons why leading architecture firms use software to manage building projects is, when properly used, the projects and people will be organized and efficient. PM software manages people and time over the course of specified project-related activities. Being able to track these variables will make sure the firms are making the most productive use of its direct hours—in other words, the hours employees and partners spend on projects, as opposed to hours spent on overhead activities.

Image courtesy of BQE Software

Software is used to manage building project progress and billing in an organized and efficient manner, tracking people and time over the course of specified project-related activities.

By integrating financial accounting software with project management software, architecture firms can maintain a clear picture of their progress on building work as well as their use of firm resources. Taken together, this can be called enterprise resource planning, or ERP, which describes the management competency while it also implies the use of firm-wide system software.

According to market researcher Noel Radley with the company Software Advice, “The size of the firm will have a big impact on the software needs. For example, a larger firm, dealing with multiple projects and employees, will need more robust project and time-tracking capabilities than an individual freelancer.” Radley recommends the following questions be asked when a firm is evaluating architectural accounting software:

▶ Can the system log hours and mark as billable or non-billable?

▶ How deep are the project scheduling/progress tracking capabilities?

▶ Can the system effectively manage costs and progress for multiple projects at once?

▶ Does the software come with solid report-writing mechanisms?

Once armed with these answers, says Radley, the firm leadership can consider how and when to make the investment.

Not Just Tracking: Marketing, Too!

As discussed previously, firms don't become a viable business just by tracking their activities and generating financial reports. They need to build business by meeting clients' needs and meeting new prospects and suspects. Yet financial planning and marketing go hand in hand.

Aside from the software, successful firms brainstorm frequently about what things they should be doing to make sure their firm is profitable. Let's assume a firm has already followed the advice given in this article and proffered by experts like Burns and Piven: They've created the firm's own operating budget (profit plan). That means the firm is positioned ideally to spend some time working on a marketing plan.

It is well understood that firms that use and follow their marketing plans are more successful than firms that don't bother creating a plan or create one but stick it in a drawer and don't follow it. A proper marketing plan should include at least the following sections:

▶ Marketing budget

▶ Image and brand

▶ Target markets

▶ Key differentiators

▶ Relationship marketing

▶ Networking and promotional opportunities

▶ Social media

▶ Public relations

▶ Fee structure

To be savvy as a businessperson, one of the fundamental traits that an architecture firm leader needs to develop is to be direct and matter-of-fact about fees. There's no good reason to be shy about asking for fees that are commensurate with the expertise and quality of service the firm provides. The firm leaders should be ready to properly present sound reasons why the fees you are asking for are reasonable and fair; with this as ammunition in hand, fees will not be an obstacle to the firm's winning a project.

“Even if you are interviewing for a small project, I recommend you rehearse this with your partner, a colleague or even your spouse so you don't go into an interview without having properly prepared,” says Burns. “If you spend more time developing pricing and negotiating techniques you will be able to be assertive and successful.”

Uncompensated Services and Other Flaws

One of the biggest flaws architects make is providing clients with uncompensated services. The firm must use solid architect-owner contracts that clearly spell out what is (and what is not) included in the fee. When a client asks the firm to perform services that are not in the contract, the first step is to bring this fact to their attention. It is at the firm's own discretion to opt to undertake the services for free the first time—“Just this one time,” they say—but the firm must also unequivocally let them know in the future you will have to charge them for any more additional services.

“Throwing the client a freebie can in fact be a good marketing tactic, but only if the client is first informed that the firm is doing them this one favor,” Burns explains. “But if you just give away your services without the client's acknowledgment, you will find them expecting free services in the future.” The first interaction will set the precedent, and this is another reason that architects often desire to become a savvier businessperson. The clients will respect their service providers for standing up for their rights. Though some clients may have nefarious aims, certainly not all clients want to take advantage of the firm leaders' better nature. Most clients are well meaning but need to have a provider with the backbone to stand up for its own rights.

One thing to keep in mind when providing free services: The standard of care and your exposure to liability are exactly the same as if you were being paid. So free services can come with a very high cost.

Here's an example of a firm that once got burned in a similar situation: The client decided to add a fireplace to a family room addition that a small architecture firm was designing for them. Of course by the time the client decided to go ahead with the fireplace, the firm had already completed the construction documents. It was a simple change to pop in a prefab fireplace, so the project architect went ahead and made the changes and got the revised sketches out within an hour. No charge. Weeks later, the firm realized that the exterior flue violated the building setback lines and it had to be removed and installed within the building. This cost money, and guess who the client expected to pay for these changes? No good deed goes unpunished.

Reimbursable Expenses and Markup

Based on visits to hundreds of architecture firms, consultants like Burns are familiar with what goes on in the architectural back office. One of the biggest areas where firms leave money on the table—beyond giving away services for free—is in their inability to capture and charge for their reimbursable expenses.

All contracts should include a clause allowing the firm to be reimbursed for certain expenses—travel, printing, messenger services, and the like. And just as important is to include a clause that provides for a markup. Many firms always include a standard 20 percent markup to expenses. While certain clients might balk or attempt to negotiate the markup, the firms are entitled to this because of the cost of overhead and administrative costs related to these expenses.

This brings the discussion back to the use of proper tracking software. With software as an ally, the firm will be certain that all the expenses incurred will be charged—if allowed by contract.

Even more so, by using proper tracking software, an architecture-and-design firm can be certain that all financial, enterprise management, and project management goals are being considered all the time. For example, if that expense is incurred, it will be charged if allowed by contract. Why? Because the trained staffer entered the data, so the tracking software now shows the occurrence and an automatic billing process will carry the charge forward.

“But wait, you're an architect,” Burns quips. “If you provide design services to create a timeless piece of architecture, why do you need to understand the business side? The main reason is so that your firm is as sustainable and healthy as the buildings and interiors you create.”

Chris Sullivan is an author and principal of C.C. Sullivan (www.ccsullivan.com), a marketing agency focused on architecture, construction, and building products.

See how ArchiOffice can help your firm. ArchiOffice takes all the disparate information you deal with and organizes it brilliantly. It makes time tracking, project management, and billing easy with an intuitive, streamlined design. www.bqe.com/CEU

|