Effective Financial Management of Architectural Firms

Reaching the Firm’s Profit Goals

Architects earn their revenue (and profit) by working on building projects. So it should come as no surprise that the most common denominator for planning and measuring financial performance is the direct salary expense (DSE). This is the salary cost of the hours charged to projects—in other words, the firm's billable time. Knowing the staffing level and overhead, a firm's profit goal can be used to determine how much direct salary must be charged in order to hit that profit target at the end of the year, according to the AIA publication, The Architect's Handbook of Professional Practice.

To illustrate, the firm can apply the sample profit plan developed above to calculate the DSE multipliers, which are numbers that can be used to determine the values such as the target break-even, profit, and revenue amounts. But in order to do this, the firm must first determine its Efficiency Ratio. The efficiency ratio is calculated by dividing direct salary expense by total salary expense. This also means that:

Direct Salary Expense = Total Salary Expense x Efficiency Ratio

So how does an architecture firm determine its efficiency ratio? They can do the math above, or they can assume a profession-wide benchmark. For example, there are statistical surveys showing that, on average, architectural firms achieve about 65 percent efficiency ratios. This averages all employees—not only principals but also all staff members—even though efficiency ratios may be different for principals than they are for interns or others. For example, national benchmarks show that principals may be only about 50 percent efficient, for example spending 20 of their 40 hours/week on work billable to projects, while architectural interns may be 95 percent efficient.

Armed with this information and the resulting ratios, the firm can modify the sample profit plan above by making adjustments to acknowledge the estimated efficiency ratio:

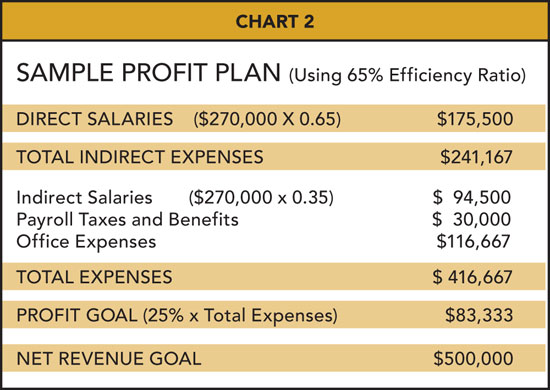

Using the results from Chart 2, the firm knows that its total salary is $270,000. But since it operates only with a 65 percent efficiency ratio, the firm's DSE or direct salary expense is $270,000 x 0.65, or $175,500. Next, the firm must determine its break-even multiplier (determined by dividing direct labor plus overhead by direct labor) and its planned net multiplier, a measure of the revenue required for each dollar of direct labor spent on projects.

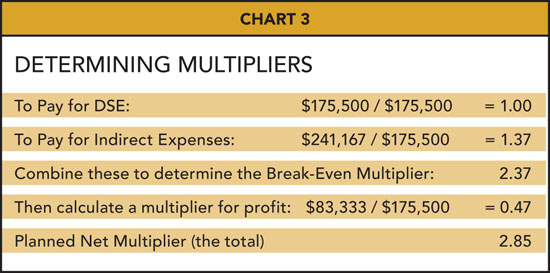

Adding together the multipliers for the firm yields the planned net multiplier—in this case, of 2.85. Like a utilization rate, this is a measure of the firm's efficiency at producing work and yielding a profit. And this is a magic number, specific to the firm. Once the firm knows it, they can make a number of financial planning decisions.

Notice