11 Top Key Performance Indicators (KPIs) of Successful Firms

KPI #6 – WORK IN PROGRESS

Work in Progress (WIP) is the value of billable time and expenses that have not yet been billed on an invoice. It includes work that has been completed, or expenses incurred, but it is in the progress of being billed. WIP is recognized as an asset on the balance sheet and as (unbilled) revenue on the income statement.

This KPI metric provides managers with information to evaluate the progress of a project. To effectively manage a project’s budget, the manager must know what has been billed and what is available to bill. This gives the manager the power to proactively manage the budget, guide billing and identify any potential overruns.

Some of the most profitable firms track the aging of their WIP. That means the amount of time that it requires to invoice for the WIP. If it is over 90 days, for example, that indicates that employees are being paid, but they bring no billable benefit for three months. It can also be a red flag that the project isn’t progressing as planned or there may be an error in billing.

KPI #7 – PROJECT COST MULTIPLIER

This next KPI focuses in on the actual performance of a project. We are calling it the Project Cost Multiplier, but it is also sometimes referred to as a Net Multiplier. Either way, this is a measure of actual performance - how much money is actually being earned for every dollar spent on direct labor. As such, it’s a measure of results and is a gauge of the financial well-being of a project and, ultimately, the firm.

There are two things that directly affect how the Project Cost Multiplier is calculated. The first is the actual employment costs which is specific to each employee, represented by the unit of 1.0. The second is the overhead rate which is the cost of non-project related expenditures (indirect expenses, including indirect labor), expressed as a percentage of total direct labor. The lower a firm’s overhead rate, the higher the profit margin - a target of 150-175 percent (or 1.5 to 1.75 x total direct labor), is generally acceptable.

Combining the direct employment cost with the overhead rate yields the actual cost of doing business. Billing at that level means the firm would just be meeting expenses so it is referred to as the “break-even” rate. If, for example, a firm has a 1.5 overhead rate, that would be added to the 1.0 employment cost resulting in a break-even rate of 2.5. More specifically, an employee with a $100,000/year salary would have a break-even rate of $120 per hour. ($100,000 divided by 2,080 hours = $48/hour times 2.5 = $120/hour). In order to obtain a 20 percent profit, then the billing rate would need to be $150 per hour.

The Project Cost Multiplier takes all of the above into account by comparing it to the break-even rate. If the Project Cost Multiplier is 1.0, it is the same as the break-even rate meaning there is zero profit. If it is greater than the break-even rate (i.e., 1.01 or more), then the firm is earning a profit, if it is less, (0.99 or less) it is losing money. Like many KPIs, the Project Cost Multiplier can vary from phase to phase. Much of this differential has to do with the costs of the employees doing the work as it relates to the billable value of their time. Hence, having the information available so it can be analyzed not only on the project and phase level but even at the activity level, helps firms learn which project types, phases, individuals, and services provide the greatest profit margin.

KPI #8 – AGED ACCOUNTS RECEIVABLE

The final four KPIs that we are covering are generally considered to be firm level metrics. However, it’s always important to consider everything within the firm at the project level since the projects are the source of the information that is being fed into the firmwide information. If something doesn’t look right or is troubling, it can usually be traced to a particular project or client where it can be properly addressed and managed.

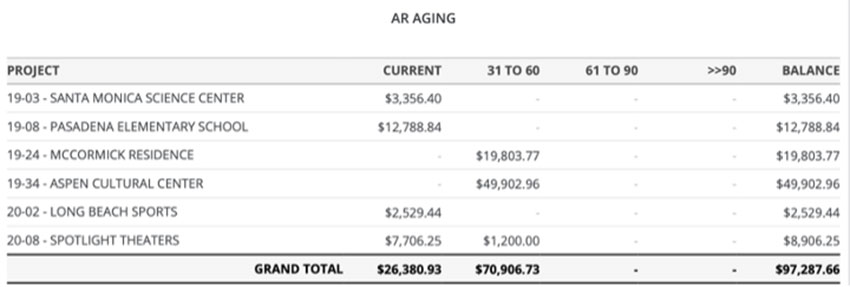

Aged Accounts Receivable shows where payments stand in relation to the due date of the invoice. When receivables age greater than 60 days, the likelihood of collections decreases.

Understanding what a firm’s net revenue per full-time employee is provides information to plan annual budgets both for expenses as well as for revenue. Prevent your firm from losing revenue.

All firms track their Accounts Receivable (i.e., invoices sent out that haven’t been paid yet) but might do it in different ways. Some firms like to calculate their average Accounts Receivable (AR) and use that as a benchmark each month of the amount of business they are doing. The annual average accounts receivable can be determined by adding up the value of accounts receivable at the end of each of the past 12 months and dividing by 12. Of course, if a firm is growing, it is perfectly reasonable to see AR grow as well. So, just looking at average AR values going up isn’t the best indicator. It must be considered in context–is the firm actually growing or is it taking longer to get paid?

The time between the date of the invoice being issued and actually receiving payment is referred to as the aging of the Accounts Receivable. Usually, invoices are considered current if they are paid within 30 days although some clients require up to 60 days to pay. Someone at the firm should be paying close attention to any aging AR. That’s because, in general terms, it’s usually very difficult to collect on invoices that are greater than 60 days old. It is a significant concern for any aged AR that are greater than 90 days since the common experience is that they become almost impossible to collect and may have to be written off. That can immediately change all the profitability and firm health numbers we have seen thus far.

KPI #9 – NET REVENUE PER EMPLOYEE

One way to benchmark a firm as compared to other firms is to look at the net revenue being generated per full-time employee. For example, in the United States, the average architectural firm yields about $151,000 per full time employee per year. So, a 10-person firm with $1.5 million in annual net revenue would indicate they are pretty much average under this KPI. Firms that are averaging closer to $200,000 in revenue per employee are likely very profitable.

Net revenue is a measure of past performance over a year─how much money did the firm bring in for itself (i.e., not counting consultants, etc.). The net revenue per employee is calculated by dividing the annual net operating revenue by the total number of full-time employees. This metric becomes useful for planning and forecasting a realistic range for future annual net operating revenue.

KPI #10 – RUNWAY OR BACKLOG

This KPI is focused on how much work is remaining in existing contracts but has not yet been completed or billed yet. Some people will simply call this “backlog,” or it may be called the “runway” because you don’t want to get to the end of your runway. By taking some data from the Work in Progress KPI and related data, it is possible to see how much contract work is remaining. Dividing that by the total monthly cost to keep the firm running indicates how long before the firm is out of work, and out of money. As a strategic measure, it is often best to subtract out the portions of the Construction Administration fees that will be earned beyond the next 12 months since that timing may not be predictable.

Determining the backlog/runway is often critical in terms of planning for future months or years of the firm operating. For example, if the analysis shows more than a year of reliable contracted work with project time schedules to match, then it is likely that the firm will be busy and potentially on good financial ground. On the other hand, if it shows only six months or less of runway, then there are really only two basic choices - either bring in new work or plan on lay-offs. Of course, some firms might take the approach that they are anticipating new work and don’t want to lose good employees until that work comes through. In that case, they might have some cash reserves to dip into and use that to extend their runway, but this carries some obvious risk. It is always good practice to maintain at least three months or more of operating reserves to carry the firm through other unexpected financial issues. So, any dipping into reserves should keep that minimum balance intact.

Notice